Speaker 0 00:00:00 The Bitcoin standard toolkit is a selection of Bitcoin services. I recommend to my readers and learners on safer dean.com as they upgrade their monetary operating system from the theater standard to the Bitcoin standard. These companies are, Nidek a leading full service financial services firm dedicated to Bitcoin, applying institutional wisdom and ingenuity to help clients access the unrealized potential of this emerging asset class Nidec offers the full suite of solutions needed for financial institutions to access Bitcoin, including custody, execution, financing, treasury solutions, integration partnerships, and more the team behind an iDIG brings decades of experience in the financial markets and passion for sound money to help provide the rails that will bring about a move to the Bitcoin standard. I have been working as a consultant for knighting for two years now, and I'm very impressed with their vision focus and execution. Go to nike.com to learn more cipher, safe, to secure your Bitcoins.

Speaker 0 00:00:49 It is important to keep your seed phrase backed up safely. And for that I highly recommend using the cipher wheel seed storage device, a gorgeous and brilliant sturdy piece of low time preference engineering from a fourth-generation machine shop in Maine. The cipher wheel is machine from solid stainless steel and its unique and elegant design is inspired by secret decoder rings as well as legendary mechanical engineer, France rule law and the golden age of machine design. If you've read the Bitcoin standard, you'll know, I think the late 19th century was a golden age for many facets of human advancement because of hard money. Bitcoin is bringing hard money back and our friends at cipher say for giving Bitcoin the low time preference machines, it deserves from the golden age of design, go to cipher, safe.io to get the cipher wheel for your Bitcoins. Okay. Coin. Whenever someone asks me how to invest in Bitcoin, my advice is to accumulate Bitcoins periodically for the long run or what is called dollar cost averaging.

Speaker 0 00:01:37 When you buy every day, week or month, you channel Bitcoin's volatility to your advantage in the long run, this strategy will outperform every other Bitcoin investment strategy probably except for amazing luck. Perhaps the best place to do recurring purchases is OK coin because they have the lowest fees for recurring Bitcoin purchases. You will find anywhere if you're stacking SATs for the long run, every PSAP matters and the fees with each purchase will add up. That's why I recommend you buy that the lowest cost possible from okay. Coin. Okay. Coin is also the Bitcoin exchange available in the most countries around the world. So it will hopefully be accessible for you wherever you are go to. OK. coin.com to get started with your stacking. Not all one as discussed in the Bitcoin standard. Bitcoin is controlled by the nodes that operated software. It is only through consensus between nodes that the Bitcoin blockchain continues to live and is only by running a Bitcoin node that you are part of this consensus and can verify the validity of the transactions you receive and the ownership of your coins.

Speaker 0 00:02:28 Whenever anyone asks me, what are the most important morning signs that something is wrong with Bitcoin? I always answer the following. If the number of Bitcoin nodes is declining and or the cost of running a node is rising significantly. I believe it is really important to run a node, but I don't recommend running it on your work or personal computer as it can compromise the performance of your computer. And more importantly, the security and privacy of your Bitcoin node a far better solution is to buy a dedicated hardware node. And for that, I highly recommend Knotel manage all your Bitcoin activity, such as lightning or BTC pay server and isolate from your personal computer by putting them into one dedicated device that is always running and does one thing only Bitcoin become a first class Bitcoin citizen by running your own Knotel node

[email protected]. And that's spelled N O D l.it finally called card. My hardware wallet of choice is the cold card. I strongly recommend only conducting Bitcoin trades on computers that are dedicated to Bitcoin and cannot connect to the internet. I like the cold card because it is a contained machine optimized for Bitcoin and Bitcoin only cold card is basically a small computer that can only do Bitcoin, which makes securing it more straightforward. Use the code Bitcoin standard on cold card wallet.com to get a 5% discount

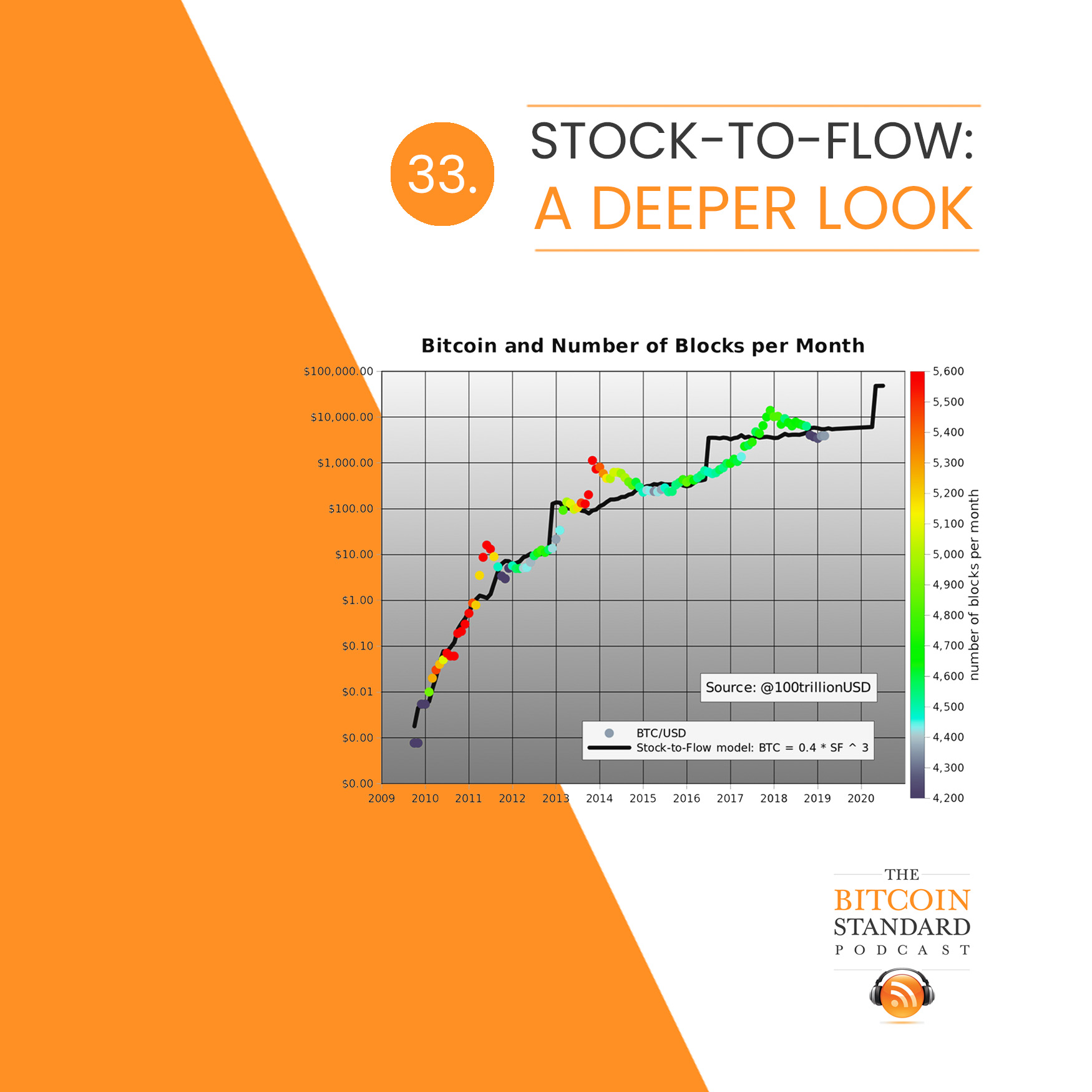

Speaker 1 00:03:38 Hello and welcome Bitcoin standard podcast seminar. In today's seminar, we're going to be discussing the concept of the stock to flow. Just something that I discussed in the Bitcoin standard. And, um, it's become a pretty, uh, popular topic amongst Bitcoiners over the last couple of years, because it seems to have proven to be a good analytic lens, uh, to analyzing the economics of Bitcoin digital currencies and, um, other currencies as well. So briefly, uh, stock to flow as a ratio is a measure of the total stockpiles of a good divided by the flow or the annual production of the goods. So it gives us a sense of the orders of magnitudes involved between the total supply of a good that we have that exists in the market and, and the annual production of this good that is being added onto the market effectively. What it is is just the inverse of the, uh, percentage growth rate.

Speaker 1 00:04:42 So if you have something whose stockpile is growing at 5% per year, the stock to flow is going to be a one over five or 20 or one over 0.05. So 20. So the stock flow is just the inverse of the annual supply growth rate. And of course, as you can imagine, intuitively this would make sense. The animal supply growth rate is likely to mean more devaluation of the currency. And so if you look at national currencies and I do that in the Bitcoin standard, if you look at national currencies, you see the, um, harder national currencies, the ones that have maintained their value better over time are the ones that, uh, have a supply growth rate ranging around, uh, five, six, seven, eight, 9% or, well, a little less, but about five, 7% more or less, but in the low percentages. Whereas the bad currencies that have had very high inflation and hyperinflation have had their supply growth rates grow at 100, 200, 300, sometimes in the thousands of percent per year.

Speaker 1 00:05:48 So obviously intuitively this makes sense if your currency is growing at an, at a percentage supply growth rate of a thousand percent, um, which happens in some places, uh, at some point in time, you'll witness very quick devaluation of the value of the currency. And so you're going to witness very high price inflation, and you're going to witness the, uh, amount of wealth that is parked in the currency and declined because nobody wants to be holding a currency that is being inflated at this rate. So a, an annual percent growth rate of 1000 is a stock to flow ratio of 0.1. Any good with a stock to flow ratio is 0.1 is not going to work as a, uh, good money. Nobody who's going to hold it. And so it's going to drop most market commodities. The stock to flow is in the range of one it's roughly around one.

Speaker 1 00:06:43 In other words, if you look at how much copper we have in stockpiles in the market, held in, uh, reserves and held by, uh, copper traders and being stored by corporate consumers. If you look at how much of that exists around the world, it's roughly in the range of one year is production. And when I say roughly in the range of one year's production, it could be 50% less. It could be 2% more depending on the dynamics of the market and the dynamics of the method itself, but more or less every year, we're making about as much as the stockpiles that we have at any given point in time, because people aren't, uh, keeping the stockpiles around, nobody likes to keep large amounts of copper sitting around. Um, if they have them there, just hold it in temporarily until they can ship them on. So for most market commodities, their stock to flow ratio is around one it's, uh, it may vary, but it's not going to vary very much for monetary commodities, for commodities that develop a monetary role.

Speaker 1 00:07:46 You're going to see a stock to flow ratio that is closer to the, that rises above one. And so the higher it rises, the more likely it is to have a monetary role. The more likely it is to be used as money in the more likely it is to store value for the future. And so we see this across metals, the only methods which have a stock to flow significantly different than one are silver and gold, that's it, silver and gold are the only metals who start to flow is significantly different than one. Historically it used to be this silver stock, the flow around 2030, something like that. In other words, you had somewhere between three to 5% annual growth in the stockpile of silver, but over the last century and a half as I like to discuss in the Bitcoin standard over the last century and a half, we see that, uh, the price of silver has gone down drastically.

Speaker 1 00:08:42 And so the value of silver has had the value of silver on the market has declined. And with that, we see, and I'm going to share here the chart of the price of silver. If you look at the chart for the price of silver over period, we've seen on the price of silver, go from, from the period from 1870, really is when the silver dumps started and it has never abated. So this is actual spreadsheet that I used for the Bitcoin standard. This is the chart there, and this is the, these are the numbers for it. You see, historically in the 16 hundreds, 17 hundreds, we were at around 15 and it was always around 15, sometimes dipping to 14, but usually 15 and the 17 and the 18 hundreds, it starts rising to 16. And that's when you know, the, the, the Canary was, uh, singing in the goldmine of silver in the mind for silver and the silver mine, not the gold line.

Speaker 1 00:09:36 It's really around 1871, 1875. Really when the, when the real decline of the value of silver begins, its thrives to 17 for the first time in 1875 and then 18 and 1876. And then it takes off into the twenties and thirties and continues to increase. Um, it has periods where it drops back down to the early twenties, but generally the trend is for a number to go up. And this is up until 27 16. It was a 73 today. I think the gold silver ratio is closer to one. It did hit one 20 since the qualification of the Bitcoin standard at some point. But I think now it's closer to 100. Um, so silver has been in a bear market compared to gold for 150 years. And it's not about to change anytime soon. And with this, what we see is that Silver's actual stock to flow ratio has been declining along with it.

Speaker 1 00:10:32 And so if we look at the chart for the stock flow, this chart, I had it in the Bitcoin standard, but I did not include the data. I did not include a table. We, I thought the chart was enough, but it should have probably included the table with the data. This shows us the stock, the flow for all these different, um, metals for copper it's, uh, close to zero. I don't know why this, um, this is not my usual computer. So now it's rounding the numbers down, but it was close to zero on, um, for copper, it's about one for oil at that time, it was 5.6 for silver. I remember the starter floor for silver around then was around 5.6. If you measured the global silver stockpiles and divided them by annual silver production, as it was around 5.6 for the Euro, it was 16 for the U S dollar.

Speaker 1 00:11:24 It was 18. And for the Swiss Frank, it was around 22. This was the average for the previous, uh, 25 years. This was the 25 year average that I took for these currencies. So it wasn't a projection and it wasn't one year. It was the average for the past 25. That's really the best estimates we can get for Fiat currency since they're not algorithmic. And then if you look at the Japanese yen, it's at 25, that does better than, um, most Fiat currencies that has a low stock to flow ratio. And then gold was at 63. So Bitcoin in 2017, right? I was writing the book. Bitcoin was at the 25 at that time, but in 2025 Bitcoin going to jump to one 25. Now Bitcoin is around 50 56 or so, depending on how you calculate, calculated how you calculate the stock to flow.

Speaker 1 00:12:12 But Bitcoin stock the floor now is around 50 56 and in 2025, after the next having, it's going to be around 125, which is going to be the highest stock to floor that has ever happened. Um, gold, we're not going to overtake gold most likely in this cycle. There haven't been times in which gold has had a higher stock to flow than Bitcoin right now. But by the next cycle, when the stock to floor rises to 125, Bitcoin is going to be higher than any monetary asset that humanity has ever seen at that point. It really overtakes all other assets. We've, we've never had a monetary assets that had a, an annual growth rate that was less than 1%. It's going to be wild. I cannot wait for this. Uh, this is, this is the situation with silver, right? And recently I thought, you know, what this discussion for today was the recent discussion that, uh, you start hearing about of people looking to pump all kinds of stupid shit points, um, thinking that, you know, if we all buy them together, then somehow we can all get rich together.

Speaker 1 00:13:24 Um, and it's, uh, I thought it would be a good time to do this. I, I, I made a threat about silver and I basically explained why I think silver is a shitcoin and this is, this is a good example of it. It's down to around six or 5.6 right now, the stock, the floor. And it continues to decline. And arguably, since then, since the book has been published, I was looking at the most recent numbers from the silver Institute. It's actually worse than that. It's now down to a three. So the stock to flow for silver is practically three at this point. And I think there is, there is a good article, which I'm going to, um, if we look at this is the data from the silver Institute. If you look at it, there's the silver report, which, um, runs the data, but it's not very, they, they have the data for this stockpiles in this.

Speaker 1 00:14:18 This is where I got data. And if you do it this year, you'll find that the stock, the flow, if they don't calculate it in the report. But if you do what you find the stock, the flow is three. Now there was an article by a guy called Yan new, and he was from a company called <inaudible> gold, where he takes issue with the silver institutes numbers on a silver and argues that the stock flow should be for silver should be between 30 and 60, rather than a three. And so I thought this would be worth bringing up and looking at it's a good, it's a good overview of the numbers. And I recommend reading this article and full seeing his argument, but ultimately based on the silver Institute, he comes up with this chart for what is the supply of silver above ground silver. And so if you see, if you look at the, here, we have a pie chart where, uh, almost 50% of the pie chart is industrial use undetermined or lost silver.

Speaker 1 00:15:23 This is about 852,000 tons. So a little less than 50%. And then another chunk, which is a little bit smaller, but also less than 50%, 791,000 tons. That's for jewelry decorative and religious purposes. And then you've got $51,000, 51,000 tons, I'm sorry of coins and 57,000 coins of bullion. So if you look at an annual production for S for silver, every year is around 30,000 tons. So what the silver Institute numbers would imply is if you wanted to look at global stock bars, you look at coins and bullion because that's, what's liquid, that's the liquid silver, that's the silver that's, um, really playing a monetary role. And so you would CA you would divide 30, roughly 30,000 tons by 108, which is the total for bullion and coins. And you would get a stock to flourish over about three. Now this article takes issue with this and says, no, you should count all of these 791,000, which is jewelry, decorative, and religious, uh, silver.

Speaker 1 00:16:42 You should count that as part of the silver stockpile. And so if you count that, then now the goal, the global silver stockpile is around 891, or about 900,000 it's around 900,000 tons. And so then 30,000 divided by 900,000 is closer to, uh, stop the flow ratio of 30. So as he says, I would suggest that somewhere between 30 and 60, if you take all bullion coins, jewelry, and silverware, you will arrive at 30. If you add the silver in industrial products, you will, you will arrive at 60. So what do we make of that? Do we agree with Mr. New house on this analysis that, do we think that this means that silver should have a stock the floor?

Speaker 2 00:17:32 Um, yeah. I mean, w what you said about, um, bullying and coins being the thing that's playing a monetary role, then that would make more sense. I mean, maybe you'd have a case for jewelry, decorative and religious. If the world went to shit, or if the, of silver just shot through the roof, then people might, um, use jewelry as, as a form of money, uh, to get some fear very quickly, but the industrial use, uh, I don't see the case there too much about that. There are my thoughts.

Speaker 1 00:18:04 I think when the industrial it's clearly out of the question, you can't read account industrial because, um, because you know, the silver there is extremely expensive to decal, so it's effectively been buried under the ground, and now you need to mine it, and it's really expensive to mine it back. So there is some silver recycling that takes place always, and it does add to the supply, but, um, you know, it's, it, it, it has to be balanced with the cost of what the cost of mining. We can't have too much recycling because, you know, it's, if, if it's more expensive than the cost of mining, it's not going to happen, though. We'll just mind that then they'll throw the silver away. And if it's much more, if much, if it's much less expensive than mining, then, um, you know, it'll happen very quickly and people will start converting the silver in massive quantities and inflate the market.

Speaker 1 00:19:00 So ultimately the cost of recovering industrial, silver, or jewelry and decorative and religious silver in my mind is effectively makes them not part of the stockpile because you can't really use silver, uh, stuff as money. And if you think about it with jewelry in particular, I think the reason you can't really count it, this because it's not liquid. And in fact, when you're buying a jewelry piece were made with silver, you're primarily paying for the production of the silver. You're not really paying for the, uh, for the stuff that's inside it. And in other words, it's, you know, you look at the average piece of silver jewelry and all of the silver that's in it is worth a few dozen bucks in best case scenario. And usually the piece will sell at the significant, um, markup to the content of silver inside it, because, uh, there's craftsmanship that went into making it in that sense.

Speaker 1 00:20:02 It's not being held as a monetary matter, it's that, you know, if it was with gold it's, it's this case, this is less clear because gold is far more valuable. You know, it's, it's about 100 times more valuable per gram. So putting 10 grams of gold in a piece of jewelry is worth roughly 100 times as much as putting 10 grams of silver, but you can only fit so much silver or gold into a piece of jewelry. So ultimately a necklace or a bracelet or a pendant, or, um, any kind of, um, um, any kind of silver or gold jewelry will only carry so much, um, monetary weight in the, of gold. That can be significant in the case of silver. It's just not, it's not as significant as the, uh, as the amount as the, um, production that went into it. And so effectively selling a bracelet that has silver is, you know, it involves a significant cost because you're actually not just selling a silver that's society.

Speaker 1 00:21:09 You're losing the necklace, you're losing the craftsmanship that went into making the necklace or the bracelet. So you can't really count it as a monetary. Good. And you can't really count it as part of the stock bottle. It's ultimately not part of the liquid market that is being bought and sold in a monetary sense. And the four that you should really look at, um, bullying and coins, as I said, because gold is 100 times more valuable per gram. You can make the argument that this is different in the case of gold, but actually when you think about it, this is also an indication of Gold's growing the, the monetization. Because if you look at gold and the data on gold is much better, if you look at gold, uh, well, the data's obviously both terrible compared to Bitcoin data, but we were taking these numbers at face value.

Speaker 1 00:22:03 If you look at gold, there's about 92,000, almost half in, uh, jewelry. 33,000 is in our official holdings by central banks. That 8,000 is in bars and coins. 2,400 is in ETFs and 27,000 is other fabrication on unaccounted. So the 27,000 are industrial uses. You could say that these are arguably outside of the stock, the flow of the stock by you could meet, you could make the argument that they aren't necessarily part of the stockpile and with the jewelry as well. You could maybe argue that maybe some of that jewelry is becoming more about the cost of the jewelry itself, itself. Um, you know, the piece and the, um, and the, and the diamonds and the other things that go into it. And just the craftsmanship that went into, uh, that's what people are really paying for rather than the, uh, gold continent. So if you think about it this way, you could make the argument that gold has a higher stock to flow, has a lower stock to flow because the stock bottle is actually lower than it actually is because a lot of it is being stuck in industry and being stuck in jewelry, where it's not very liquid and it's not liquid as gold.

Speaker 1 00:23:15 You can just take that piece of jewelry with a few grams of gold and, um, expect to sell the gold. You, you have to find somebody who's going to be buying the jewelry and the say diamonds or rubies that come along with it. Uh, so the whole piece, so it's, it's not really a liquid part of the market. It's not, you can think about it as, um, part of the stockpile. And you can't think about it as being held, um, as part of the stockpile, bringing it to market for its holders to be, to sell it. It's, it's not liquid, it's not in barns, not in bullion. So you could arguably maybe say the same applies for gold. Let's talk about for gold would necessarily would you should be even lower, but in the case of silver, I think, you know, the, the, the proof is in the pudding.

Speaker 1 00:24:03 If you look at the history of the price of silver, you know, with all of these squeezes that they keep trying to do, we see how the price of silver just continues to plummet always. And so they try to do the silver squeeze last week, where they said, let's all buy silver. And then, you know, we'll spike silver, and the banks will go bankrupt. And we'll somehow, you know, we'll destroy wall street because we'll make them run out of an industrial metal. Um, it's, it's ridiculous because, you know, the production of silver can be ramped up there easily. And, um, the recycling can be ramped up and you can bring significant stock onto the market and depress the price. So there was a very quick pump from around 25 and a half to around 29, but they've crashed back down. It's entirely possible that they might get a short squeeze happening and that it would spike.

Speaker 1 00:24:56 Um, we could see the price go up significantly. If you look at data, you know, it's, it, it can go up and particularly, you know, with when you measure it in national currencies, there is, um, there is the possibility that it can continue to go up. If you look at, uh, the chart all years, you know, it's, it's, it's significantly up or since 2000 significantly since 1980, significantly up since 19, uh, forties. Um, but not that significantly up since 1917. So it's really been a bear market for a hundred years. Uh, more or less facility even measured against the dollar. So they were at 26 and back in 1916, 1917, it was at 18. So 26, 18 to 26 is pretty abysmal and that's even measured in dollars. So the notion that silver can significantly rise, I think is ridiculous. And we see it happen over and over again.

Speaker 1 00:26:06 You know, we see these silver spikes in the seventies, there was a big spike. And then the hunt brothers, the story that I discussed on the Bitcoin standard, they sparked the price up significantly. Oh yeah, this is adjust for inflation. So, um, you can ignore what I said about 1915. It was also, it was probably much cheaper in 1915. Um, but there's, this is adjusted for inflation. So yeah, it has gone up against the dollar. Um, but it definitely has not gone up against gold. And so this was really why I think silver is a fool's game because it's all of the disadvantages of gold with, uh, with, with, without the only benefits. So you're getting, as if you look at this chart, you see this, uh, always basically falling against gold. It gets a few spikes where it rises, and this is the gold, silver, silver price ratio.

Speaker 1 00:27:01 So the higher, the number, the more valuable gold is, and the less valuable silver is. And so you see, it's just been a nonstop trend. Upward silver continues to devalue against gold. And this is, I mean, you know, these are two commodities that are sold and bought all over the world. People buy and sell silver all over the world. It's easy to see many population, but ultimately you're talking about 150 years of people from all over the world, mining gold and mine, silver and buying gold and buying silver and selling all the selling silver. And these prices have held through billions of transactions over a century and a half. And the trend is unmistakable. Silver is becoming worth less and less and less. And I think it's inevitably, it's both a cause. And consequence of it's constantly increasing the constantly decreasing stock to flow ratio.

Speaker 1 00:27:50 So because it starts to lose monetary premium and it starts becoming less and less valuable as money. It becomes less valuable and real in terms of real goods and services. And so it becomes more economical to be used in things other than money. So you start seeing and seeing it in, um, you know, tea sets and you start seeing it in industry showing up in all these places. And then that effectively means that you're eating away from the stock box. So it becomes an industrial good in that it starts getting consumed. So once it starts to get consumed, you're eating from the stockpile. That's when the stock, the flow begins to decline because the production starts getting ramped up and the stockpile is being eaten down and the good is becoming an industrial blood. And I wonder if we're seeing the same thing happen with gold now, because if you think about it in real terms, gold is probably not keeping up with inflation.

Speaker 1 00:28:42 Like gold is still at 1800 right now. And, you know, we've seen an enormous amount of like, if you measure, um, gold in terms of keeping up with value, um, with other, um, monetary assets, you know, it's barely keeping up with the us dollar and the us dollar is massively getting inflated and losing value against hard assets at all times, as we see. So it's arguable that gold is becoming worth less and less as a part of the global economy. So the value of gold is declining because it's not, it's not growing as much because it's not getting monetized as much because people aren't moving to gold people, aren't moving to golden, very large quantities. And the supply of gold is increasing. And so arguably the price begins to decline in real terms, and that leads to more utilization in industry. And therefore that leads to stockpile declining.

Speaker 1 00:29:44 And then that leads to diminishing stock, to flow ratio that leads to the good, becoming more of an industrial good and less of a monetary. Good. I think we are seeing this happen with silver right now. If you look at the numbers for this year, as we did now for silver, you see the stock flows closer to three. So in the, in the last four years, as I was writing the book, I, when I wrote the book, I think it was 2016 data. So from 2016 to 2020, or we've had a decline in the stock, the flows from five one six to about three. So I wonder, you know, 10 years from now, maybe silver stock flows closer to one, and the price is, um, you know, not significantly different from where it is right now. It could become an entirely industrial metal. And I can think of a similar scenario of why you could say the same about gold.

Speaker 1 00:30:33 I could see the same happening to gold. I can see the beginning of, uh, the process of demonetization gold happening because let's face it. Gold is not growing in value in a way that allows it to continue to be hoarded in large enough quantities to keep the stockpiles, the liquid stock by large enough to continue to be insignificant compared to the flow. And that's why I really think it would be, it could be that it would lose its, uh, it would be lose its, um, monetary role. It, if it would happen, the point of trying to say is if it would happen and it would be because of declining demand, not increasing supply. And so this, this keeps getting, um, being brought up a lot of Bitcoiners, like to make the point that, um, gold is not going to work as money because you know, we're going to be mining asteroids.

Speaker 1 00:31:25 And when we mine asteroids, we are going to be bringing large quantities of gold into earth and then gold will become cheap. And this, I think, uh, completely misses the point of why, uh, gold is money. It's not about the, um, it's, it's not about the rarity of gold. It's about the stock flow. It's not about how much gold there is or how much platinum or silver or, um, dollars there is. It's about how much there is as a multiple of how much is being produced every year. In other words, it's about the stock deployed stock to floor, not the absolute sizes of the stock and the flow. That's really the, what would happen. Uh, if we will, we were to have a meteor or asteroid get mined for enormous quantities of gold. I guess we could imagine two scenarios, one scenario in which we just get a meteor, hit the earth and it has, um, say 200,000 tons of gold.

Speaker 1 00:32:25 So as much gold as we have hits the earth in one day, you know, one giant rocks falls on earth, hands made entirely of gold. Um, or it has 200,000 tons of gold in it. Well, okay. So, and imagine we don't have, um, we have a very smooth distribution where it, one guy owns it and decides to keep selling it, um, minting it to bars and selling it on the market. So initially what's going to happen is that the minting of gold is going to bring the price down, but say he manages to sell all of his 200,000 tons of gold in a month or a year or whatever. And then what happens? Well now we've run out of this new source of gold and how much new gold is being produced. Still the minds, the, you know, Earth's minds outside of this meteorite is still producing the same quantity of gold that they were producing roughly before this media or hit.

Speaker 1 00:33:23 And so roughly the stock flows, I'm going to double actually, because now we've doubled the stockpile because all of this new gold has come into the market and now miners have less of a, uh, of an impact on the price. So once this is absorbed by the market, then, then the next step is that gold just increased its monetary usefulness because its stock pile has become larger and it's flow has remained relatively constant. And so the increase in the stockpile has led to an increase in the stock, the floor. And so a couple of years down the line gold ends up actually being a better money. But in reality, of course, we're not going to just get this one time boost from heaven, where we're going to be getting all this giant amount of gold being sold on the market. If you're going to think about it logically, you know, um, you know, first of all, we don't know how to mind asteroids other than in Hollywood movies.

Speaker 1 00:34:27 Uh, no matter what people like to say, it's not being done for a reason. It's completely, um, uh, well, you know, I'm not, I'm not going to say impossible or insane, but there are much cheaper ways of getting gold going onto it. Asteroid it's, it's a really, really, really, really expensive uncertainly. Like there are much cheaper ways to just dig deeper into a gold mine. It's far cheaper, far safer, far more reliable. And it's been done for thousands of years by humans. They know how to do it. So the notion that we can take an entire gold mining operation and stick it on an asteroid shooting through space and then, um, take off with all the gold and bring it to home to earth. I'm not going to say impossible. I was just going to look at it, economics of it, it's completely, uh, and it's an, it's an entirely different level of expense to what we have right now.

Speaker 1 00:35:28 The methods that we have for mining, uh, for mining gold. So if it were to happen, you know, if we were to discover this enormously cheap of doing it, then the result is it's going to be also done roughly at the price of, um, you know, at the market price more or less. And, um, you know, as it starts to scale, as it starts to increase and as the production begins to increase, um, not much different happens other than the fact that more production comes onto the market, the stockpile increases. And then the new production continues to remain a small fraction of the total supply. In other words, what gives gold its monetary edge is the fact that the supply doesn't leak the stockpile doesn't leak the stockpile doesn't decline. So as long as you find more ways of producing gold, you're not going to the monetize it by finding more ways of producing gold, you're just going to dump it on the market and increase the stock pot and therefore lower the stock, the flow.

Speaker 1 00:36:37 And it's kind of counterproductive because we know the more you produce the more the stock. So then the more, the, the, the quantity that you produce becomes a smaller fraction of the stockpile. So what keeps gold, what gives gold its monetary role is not the fact that the stockpile is not increasing. It's specifically the fact that it's not decreasing as long as the stock price is not being decreasing. It's not being decreased because gold is not being consumed. Then the stock to flow ratio is rising and the monetary nature of the good continues to increase. But when you start utilizing golden industrial uses, when you start using it for things other than monetary uses, you're effectively eating into the stock value effectively, making it less and less monetary and effectively making more and more of an industrial goods. And that's where the stock, the flow begins to decline. And that's what takes away its monetary,

Speaker 2 00:37:33 Which is completely opposite to what mainstream economists or market analysts would have us believe. Right? The, the usual narrative is as there is more, a greater need in industrial usage for gold, there will be a greater demand for gold. Therefore the price of gold will go up that, you know, it's again that, you know, logically thinking through like a Bitcoin lens just turns all of that narrative on its head is so amazing.

Speaker 1 00:38:02 Yeah. And you know, if this was the case, if a lot of silver bugs and gold bugs will tell you, well, you know, you can't build batteries or this or that without silver or gold and you need this. And if it was about industrial uses, then copper and nickel would be the monies of the world. It isn't, there's the reason that nobody uses copper and nickel is money anymore. Copper is, has been demonetized even for many years before silver. And that reason is that the stock to flow is very low. The quantity of the good is constantly being consumed in industrial uses and being taken off from the liquid market. And therefore there's no possibility for the monetization of this. Good. And this is really where it comes back to the silver squeeze story of why this is really very an instructive lesson. There's no potential for a supply for a market squeeze in silver, in the long run.

Speaker 1 00:38:55 Every pump is going to dump afterward because the quantity of monetary energy that is stored in silver to use a sailor terminology, Michael terminology, the quantity of monetary engine is stored in silver is constantly leaking because constantly silver is being used in industrial stuff. And therefore the quantity of monetary energy is not large. And therefore when this quantity arises, it's very trivial for the miners to bring enormous new quantities of silver onto the market. And therefore managed to take back a big chunk of this, um, of this monetary premium back into the minor. So always whatever ha whatever happens, you know, all of these, um, all of these shit coins, really, they can't continue to hold a pump because as their price pumps, it's very trivial for their producers to make more of them. It's very easy for silver miners to make more silver, all the gold, all the silver that is being held.

Speaker 1 00:39:55 This is really what think about it, the way to think about all the silver bullion and silver coins that are held by all the silver bugs in the world are worth the production of about three years of silver. So the miners can already make a third of it. So if you double the price, the miners are going to still add at least a third more or less next year to all of this bull in and coin. And then the recyclers are going to add more and more. And the more the price rises, the more they throw in, there's no limit to how much they can keep digging under the ground and finding more silver and dumping it on the market. And of course, silver, silver bugs and silver shells, and have all kinds of stories about, um, how this actually, uh, a structural deficit in the market for so long.

Speaker 1 00:40:43 But of course the price shows, this is nonsense. There's no deficit. And the reason governments went off the silver standard is because they were printing much faster than silver was growing, but it doesn't mean that silver isn't growing. The supply is always growing. The value is always declining. It's dropping against gold all the time, and it's just becoming more and more abundant. You see it, you know, um, people don't really use jewelry, silver in jewelry anymore because it's too cheap to be used in jewelry. Even people would like the color of silver are now you get gold, you have white gold. That looks like silver, but it's actually made out of gold because people don't like silver. It rusts. There's also that. And of course, as a monitoring medium, it's completely useless because it's very, very cheap. And that's really the thing that, uh, you know, if you, if you wanted to buy significant quantities of silver, it requires significant storage.

Speaker 1 00:41:32 And so the notion that the world is going to run on a monetary standard where, uh, where, you know, $1 million is going to require, I think it was 13 bars, each one of these, uh, silver, good delivery, gold bars. I forget the exact number, but it's, it's, it's a pretty large area. You need basically a small room to store a million dollars of silver and that's just extremely expensive. And of course, moving it around is extremely much more expensive. So it's conservatively a hundred times more expensive than gold, but, um, potentially even more, uh, because it's by weight, it's very, uh, you know, gold is 100 times more valuable. So this idea that you're going to just get enough monetary premium in people holding this for the price to rise, I think is foolish thinking. And you know, the reason I like I don't like to shut up about it is because it, you know, even though some of these people might think of themselves as being motivated by sound money and wanting a free market and money and all of that stuff and, you know, let the market decide, no, the market is very clear and there's not going to be a way of restricting the supply of new, uh, silver onto the market.

Speaker 1 00:42:46 And so the people who are selling silver are going to benefit from selling it. And, um, the people who enter late are going to end up holding giant bags of worthless rusting metal. And, uh, it's, it's just another stupid shit going. And really at this point, pumping silver, I think is, uh, kind of irresponsible given what's been happening with its price and given the dynamics of the market. And I think if you look at it in terms of stock flow, it makes it very clear.

Speaker 2 00:43:14 Can you even really genuinely think of silver as an inflation hedge, if those people that are looking to store silver, like that amount of silver that you're talking about, then they're the kind of people that would be using Michael sailors kind of metrics of 20 to 25% inflation. Yeah.

Speaker 1 00:43:34 And so 20, 25% inflation, Silver's doing around 30% of inflation. So if these numbers are correct, the 30% I could, you know, I'll accept that they're, uh, wrong. Obviously there's a huge amount of uncertainty over all of these numbers because you know, they don't have full nodes. It's primitive, monetary technology where you're buying a part of something that who supply you don't even know. Um, but it's much cheaper to store gold and gold is much more likely to hold onto its value so I can understand the case for holding gold, but I see absolutely no case for holding silver. The cost of holding it is enormous. The, and the fact that it's taught hard to stock the floor means that, um, the cost it's likely to decline. And then the cost of moving it around is really insane. Like if you wanted to hold any, uh, somebody sent me a message actually on Instagram.

Speaker 1 00:44:26 Uh, they told me they heard, they saw my tweet on Twitter and they told me, I, you know, in my tweet, I mentioned a million dollars in silver, how much volume it would take. It would need basically a small, uh, uh, room to keep it in. And he told me he had a hundred thousand dollars towards in silver and they had to move a house once. And it was, and it tells me how much of an ordeal it was. It was an entire day's work to move $100,000 of silver from one basement to one another. And he tells me, you're absolutely correct about this is it's. It's insane. If you think about it, when you start putting in serious amounts of money, it's extremely immobile. It's extremely heavy and extremely cheap. Therefore you need to carry very large, very heavy quantities to move it around.

Speaker 1 00:45:18 So if you think about it this way, I can't see people holding it and real quantities and real large quantities. You know, nobody who's got millions of dollars is going well. Obviously many people will, but not a lot of people who have millions of dollars are going to be buying millions of dollars of silver and going through then the pain of holding them to emphasize this point on stock to flow. One of my favorite examples is, uh, three other metals that have been discovered that are also indestructable like gold, but they have failed to command any kind of real monetary premium. Some people dumped them on investors telling them this is the next goal is just like, they dumped shit coins telling them this is the next Bitcoin. These are platinum palladium and Iridium. These three metals have been, uh, have only been discovered recently and they have a, and this is here sharing the lectures from economics 12.

Speaker 1 00:46:17 Uh, no, sorry from economics 21 from the Bitcoin standard lecture to in economics, 12 Bitcoin standard this year registered for the courses on the website on seventeen.com. You can access all my courses and see the class notes. And this one is lecture two in Bitcoin in Bitcoin standard economics 21 course. And if you're not registered do register in the lots of courses and, um, good, uh, Austrian economics material that you over. So in this course, I go over the discussion of, um, the stock, the flow. And then I explain why gold, what gives it? Its monetary role is not so much its rarity in this cost across the earth in as much as it is the fact that it is indestructible. And we have had a very large stock accumulate. And this is something that platinum palladium and Iridium cannot recreate because they only were discovered in the 18 hundreds or so.

Speaker 1 00:47:15 And therefore all the production that we can make of them is relatively large compared to the stockpile because we've never had a very large amount of stockpile of them piled up as we do with gold, because with gold, we've been mining gold for thousands of years and that gold has been accumulating basically for thousands of years. So if you look at these platinum, for instance, is a very good example because in the 18 hundreds and early 18 hundreds people discovered and started producing a platinum, its stock bars were pretty small. When the Russians decided in 1820s to produce a platinum based ruble, they decided, well, platinum is like gold and it doesn't throw us that it doesn't ruin like gold. So it's going to be, it's shiny like gold and liters like gold. So, you know, as we know all that glitters is gold and therefore let's base our ruble on platinum.

Speaker 1 00:48:06 And so they introduced this in the 1920s and the 1820s, but it was discontinued by the 1840s. And I think in, in as explaining the notes, they misunderstood the value proposition of gold as being goals, rarity. And so assume that platinum being greater would be a better money, but the value of platinum fell on the global markets as new technology began to be employed in its production, allowing increasing new production. So even if these metals are indestructable, they do not have the many thousands of years of history of production behind them. That gold has, which makes their stockpiles much larger than any new flows. And that's ultimately why trying to monetize those things is few times we are not producing them very large quantities because we don't use them as money. So we're only using them industrially. If people started to buy them for very large quantities in order to make them into money, as the Russians were doing the 1820s when they were buying platinum and minting it into coins, yes, it's going to raise the value of platinum on the market.

Speaker 1 00:49:03 The price of platinum is going to rise, but then what's going to happen. Platinum, mine, that a gold and a lot of more platinum comes on the market. There's going to be a lot more platinum. And since there's only a small stockpile gathered over time, it's going to more or less the stock to flow will decline because the new production is going to be very large compared to the stock pass. So this has prevented platinum and palladium from ever rising in terms of the amount of monetary energy that's stored in them. And if you look at the data for their stock to flow at this point, it's closer to one for both. Metals depends on the data and it's not very reliable data for them, but it's pretty clear that the amount of production every year is equal to the global stockpiles because, um, most of the, uh, current production gets used in industry. It's get in these metals

Speaker 0 00:49:54 Get used, um, in, in, in highly

Speaker 1 00:49:57 Sophisticated electronics and the machines and all kinds of things.

Speaker 0 00:50:01 So effectively, we're putting it back in earth, wood, digging it back in when we, uh,

Speaker 1 00:50:07 Utilizes it in industrial users. And so the total amount of monetary value stored in platinum and palladium today is enormously insignificant. Very few people hold bars of palladium and platinum. And if they were to do it as the Russians had done in the 1920s and the people tried to monetize it, we're just going to end up with story like the hunt brothers, because there isn't a lot of stock bars of liquid palladium or platinum on the market and the miners are going to dump large quantities of a ton of market and it's going to come crashing down. So again, the dynamic with metals and gold is very similar to Bitcoin and shit coins. You see, you hear the same, uh, justifications for shit coins, as you would hear for, um, metals and speaking of shit coins, the latest kid on the block, um, this, uh, social media influencer by the name of Elon Musk, he's some kind of, uh, Twitter influencer.

Speaker 1 00:51:08 I think I'm not sure what exactly he does. Oh, no, wait, I am sure he's got this, um, recipient of, uh, he runs a corporation that basically trades carbon credits and loses money, making cars in order to, uh, make money on carbon credits. This guy has been pumping this new coin and, um, um, obviously, you know, just like any other shift coiner, they're very enthusiastic about their economic ignorance and, um, presenting this information. So let's take a closer look at this shitcoin and analyze it from the perspective of it's stock to flow. If we look at doggie coin or doge coin, uh, whatever the fuck they call it. Uh, the circulating supply is currently at 128 billion, which is, um, you know, a lot of those, uh, obviously as we know, the total supply of money does not matter what actually matters is the growth rate.

Speaker 1 00:52:10 And so let's try and find out what's the growth rate for this. I should coin. So looking at their Wikipedia page tells us dope cone started its initial coin production schedule with 100 billion coins in circulation by mid 2015, the 100 billion Doby coin had been mined. And so, you know, they ran out of new production by mid 2015. And so their stock, the flow had reached infinitive by mid 2015. So they'd actually, you know, they didn't really have a plan for it. So they ran out, they said, we're going to have 100 billion coins. And then they mined all of these because there's difficulty adjustment is clearly, uh, stupid, uh, no matter how they're running it. So they ran it and then these coins. So they started making more. So they decided, all right, 100 billion is clearly not enough. We need more coins. And so they started adding 5 billion coins every year.

Speaker 1 00:53:01 And so that's why we're at that level right now. There's currently no implemented heart cap on the total supply of doggy coins. Initially Doby point had a supply in limit of one, a billion coins, which would already have been far more coins than the top digital currencies were allowing. As you see there, Wikipedia is run by economic ignoramuses because they think the total number matters. And they're quite happy that they have 100 billion, which is much more than all the others. Nonetheless, in February, 2014, doggy coin founder announced that the limit would be removed in an effort to create a consistent reduction of its inflation rate over time.

Speaker 3 00:53:36 And so now what they're doing

Speaker 1 00:53:38 Is 5 billion a year forever, which actually, if you think about it is not, uh, that inflationary because as the, you know, the supply, the, the flow is constant and the stock market is to increase. So then effectively, eventually the stock, the flow goes to zero, but this is still a shitcoin even though. So currently, if we look at it, Trent, um, supply, so this year started off with 128. So 5 billion over 128 is around, I'd say 4% or something like that as 4% annual growth, um, about 4% annual growth. So it's that, uh, hi, well higher than Bitcoin, but it's not that high. It's not terrible, but of course the problem I'm with stupid shit coins like doggie coin is that there is absolutely no guarantee for the supply to remain at what it is. They've already changed the supply once. And it's quite easy to manipulate the currency and change the supply again.

Speaker 1 00:54:43 And if this thing does indeed become, um, a popular thing and it does catch on, it doesn't matter how eventually they're going to be getting into problems of monetary policy and who gets to decide on monetary policy. And eventually they're going to, they're going to have probably compromises about their supplier changes, uh, for the supply it's trivial for any shit going to be compromised because none of them has the track record of Bitcoin in terms of resisting change. Nobody ever got to change any of the important fundamental properties of Bitcoin in this regard. And so ultimately there's a limit to how much idiots exist, who are willing to trust a part of their wealth in a currency whose supply is arbitrary. And ultimately, no matter how far it goes up, it's going to go down because more and more coins are going to continue to be made.

Speaker 1 00:55:37 And they need an increasing number of people to continue the buy in, in order for the coins to continue to hold value. So eventually that's not going to hold and eventually it's going to crash. And eventually all of these stupid influencers pumping those stupid shit coins are going to be made to look very, very, very stupid. It's, it's, it's pretty, uh, absurd. When you think about it, they know that he's got 45 million followers or something on Twitter. You know, a lot of these people idolize this guy. So a lot of them are actually going to pay attention to this scam coin, which is up and in an ungodly percentage over the last few days. So it's tempting to think that, well, Bitcoin can go up and can keep pumping. So then why can't we pump any of the other coins? And of course, if you've got a, a cult of personality around you, then you can, uh, you, you can see how you'd want to be the one in charge and the one on pumping a coin that is different from the one that everybody else is using. Um, so good luck to all of the people who are going to strap on, uh, this shitcoin rocket. Um, we know how it ends up Daniel.

Speaker 2 00:56:44 Yeah. I just want to say something on this as well. You know, it just pisses me off what he's doing. It's just so freaking annoying and it just undermines everything that people like yourself have already done in this space. You know, your, your books, other people that are in this space that are trying their best to, to educate people about, you know, Bitcoin and what Bitcoin is. And just to have someone come in and just like act this recklessly is really kind of undermining every, all the hard work that many of us have been putting in for the last couple of years. So it's just really fucking annoying and not, not well-played at all. Uh, I'm sure Elon would never hear this, but you know, if he ever does like, just cut the shit and it a point I made the other day as well on a different show.

Speaker 2 00:57:35 It's like these shit coins, they need influencers, whereas Bitcoin has educators and that is such a fundamental difference between Bitcoin and anything else. So if anyone, you know, just check who you're following, right. Um, and if it's an influencer is almost certainly, well, we know it's a shit coin, it's an educator, it's Bitcoin. And, um, and I, I'd just like to point that out and, um, hear your thoughts about that as well, because it certainly cheapens everything that, um, so many people have put in place or that all the authors and whoever else, the content creators that are trying to help people understand Bitcoin.

Speaker 1 00:58:20 Yeah. I mean, I think it's, um, uh, I tweeted about him earlier today and that it's, uh, it's quite a damning indictment of Fiat that this is, uh, this is what it takes to be the richest man in Fiat. I think, you know, under the gold standard, the elites and the people who were the richest people in the world would definitely have not been doing something so crazy. You know, you think about Rockefeller, for instance, in order to become the richest man in the world, he invented modern oil. And of course it's very fashionable for, uh, the same kinds of people who pump stupid shit coins like doggy coin to hate on oil because it emits a small particulates in the atmosphere, but none of these people have tried living one year without oil products. And if they have, they would be highly unlikely to survive it.

Speaker 1 00:59:11 Um, the fact of the matter is our world is highly dependent. Our modern survival and civilization is highly dependent on oil, not because of an evil conspiracy, but because oil is nature's perfect cheap battery people. Aren't always fantasizing about creating new battery technology and the batteries are there. They're called gas canisters. They're called gasoline tanks. These things are nature's most amazing batteries. They've, they're cheap and you can move them anywhere and you can have enormous amounts of power on demand 24 seven from these things. And this revolution really gave us the modern world. It gave us the expectation of surviving winter as a given, um,

Speaker 4 00:59:59 Rather than, uh, as

Speaker 1 01:00:01 An ordeal that required you to, uh, spend your summer, um, gathering wood and, uh, hoping that your re your roof holds on the, um, on that receding holds up to the storms. It's, it's made modern homes safe and it's made, um, it's given us all, you know, and, and, um, we've had an episode here before we hosted the Alex Epstein. I highly recommend it. Uh, he, he makes the moral case for fossil fuels. You know, this, this is what it took to be the richest man in the world a hundred years ago, you had to revolutionize the world's technology for 100 years further. And, uh, you know, I'm going to piss off a lot of people here, um, who like Elon Musk, but Elon Musk has made a, uh, a car, which is, um, you know, it's, it's, it's still far less than 1% of all the world's cars.

Speaker 1 01:01:00 So he's still not cracked 1% of the world's car market. And he's not yet managed to turn a single, uh, profitable quarter without, um, without subsidies and, um, carbon trading, essentially, essentially the car business is losing money and he makes his money from a carbon trading, which is a big gigantic scam. Um, and of course the hilarious thing about it is that he uses the money from the carbon trading to finance his, um, car company and, uh, to finance his space exploration company. So the end result is that you have rich people driving cars that are subsidized by people who, uh, drive, uh, gasoline cars, because they have to buy credit, uh, indulgences from the carbon indulgences, from the church of carbon. And these indulgences are handed to Elon Musk so that he could then give people all these cars that require enormous amounts of soul, of, um, fossil fuel energy to produce, you know, the notion that we could have a Tesla car without fossil fuels is ridiculous.

Speaker 1 01:02:08 It's an entirely, um, it, a car is like that entirely dependent on enormous amounts of fossil fuels for all manners of, for, for the entire production process, from the mining of rare metals, all the way to the transportation of the metals, all the way to the, um, production of the battery and all of those things entirely reliant on fossil fuels and, um, yet, um, presented as an alternative to fossil fuels and, um, then takes all of these, uh, tall takes all that money invested in a space company, which blows up rockets all over the world. And each one of those rockets probably emits more carbon dioxide than all of the cars of the world, or at least the cars of the U S during the time of its flight. If you think about it, you know, I, I don't, I haven't run the numbers, but if you were to calculate how much carbon dioxide emissions, those things that make, um, I'm, I'm, I'm going to go ahead and take a wild guess and say that his rockets do not run on solar energy.

Speaker 1 01:03:16 Um, I think it would not be very feasible to make all of these explosions on solar or wind. I don't quite see wind turbines powering all of these rockets. I'm guessing it's high-grade jet fuel that blows up. So it's pretty amazing that he's made a business out of selling carbon credits to apparently reduce the amount of carbon emissions, but ultimately his cars probably make much more emissions in terms of production than, uh, regular gasoline cars. Because, you know, you look at regular gasoline cards, they have, they can be made so cheaply at this point, you know, you can buy cars for a few hundred dollars in parts of the world, new cars that are being rolled out for a few hundred dollars, because that technology is enormously cheap and Tesla cars cannot be sold for $30,000 without government subsidies and carbon scam credit, uh, indulgences.

Speaker 1 01:04:12 Uh, so the notion that this is the future, that this is going to eat the fossil fuel car, I think is ridiculous. And, um, you know, usually I, I, I've always held this opinion and there's no amount of pumping of the Tesla stock that can change this. What would really change my mind on this is to see, uh, electric cars. I I'm succeeding in the market, eating a very large share of the market without subsidies. So if we get to a point where we see electric cars exceed 10% of cars on the road, and they are not receiving favorable subsidies from governments, I will admit I'm wrong until then. It doesn't matter how much you pump the stock of your carbon credit trading company. Uh, you're just another shit coiner, I'm sorry. Um, and, uh, pumping doggy coin is really in my mind, the, um, it's, it's the cherry on top for what, what a Fiat, um, mind looks like in that, um, you know, he's produced, he talks about colonizing Mars, and he talks about, he talks a big game about all kinds of things and his car company still can't operate without, um, subsidies and carbon credits.

Speaker 1 01:05:33 And he falls for stupid shitcoin scams. You know, John D Rockefeller changed the world, and I promise you, he would not fall for a stupid shitcoin scam, like doggie coin. So, yeah, he's not thought about this from the perspective of the stock, the flow clearly. Um, but, uh, we'll see, we'll see. Maybe, maybe he's right. Maybe he's the genius and maybe no-gi coin is the future because, you know, he made a, he made an interesting argument today. He said that, you know, Bitcoin is deflationary, uh, to a fault, whereas, um, doggy coin is, uh, uh, has, has declining inflation. So maybe he's right. Maybe we will live in a future of electric cars and Doug Collins on Mars. Maybe I'm an idiot and we will have that happen. So we'll see On that note, um, I guess that's a good place to, uh, wrap it up now. Thank you so much guys, for joining us and thank you for, uh, all your questions. And, uh, I will see you on Thursday for the next seminar. Take care.